Update 2026: The financial aid landscape, including the options for federal loan repayment assistance programs, has undergone many changes since this post was originally published in 2017. However, I will keep this post published, as I believe there are general principles that may nevertheless be helpful for future readers.

As the first person in my family tree to attend law school, I didn’t have the luxury of pursuing higher education debt-free. However, I know I can, and will, make a positive impact in the world, and I see my debt as a reflection of how much I believe in myself to make this happen. And at the end of the day, I’m willing to put in the time and effort to make the financial investment worthwhile.

If you’re thinking about whether you should go to law school generally, click here to read my first post.

Otherwise, read on for the top 8 things you should know when weighing the financial aspects of law school.

(1) Sticker price of law school

I’ll start with the depressing news. Not surprisingly, law school costs a pretty penny.

For example, Penn Law’s 2017-2018 tuition is $59,382. Adding on fees, health insurance, housing, health insurance, and more, the total cost of attendance for the 2017-2018 academic year adds up to $87,984. Multiplying that by three years (and ignoring the not-so-slight tuition increases that occur annually), the total cost of attendance of a Penn Law three-year JD education is $263,952. A sizable chunk of change!

The same applies for public universities. Berkeley Law’s cost of attendance for the 2017-2018 nine-month academic year is $81,957.50 (California residents) and $85,908.50 (non-California residents). University of Virginia Law’s 2017-2018 cost of attendance is $84,480. For UT Austin Law, $73,831.

You get the idea.

(2) Law school ranking & metrics

It’s absolutely critical that the law school you attend can help you achieve your employment goals. I can’t emphasize enough how helpful it is to seek out people working in the career(s) that you may be interested in, and to have honest conversations to help curate your path through law school and beyond.

Look into whether alumni from the law school(s) you’re interested in have been able to pursue the type of career you’re seeking. I consider the best resource to be current or recently graduated students, since they can provide you with up-to-date and (hopefully) honest information about their law school’s job prospects. You can also reach out to each school’s admission office and ask them to put you in contact with relevant alumni. Feel free to read online forums, but like any anonymous Internet forum, take everything that is said with a rock of salt.

Also, be vigilant about checking bar passage rates generally as well as for the specific law school(s) you’re interested in. After all, even if you graduate with flying colors from an ABA-accredited law school, you legally cannot practice law until you pass your state’s bar exam.

(3) The reality of post-law school employment prospects and salaries

Regardless of whether your primary goal is to work in “big law” right out of law school, I personally would caution against attending a non T-14 law school. (T-14 refers to the top 14 law schools in the nation as ranked by U.S. News & World Report.) It’s certainly possible to find a job that is both personally, professionally, and financially satisfying from non T-14 schools, but the journey is undeniably more difficult.

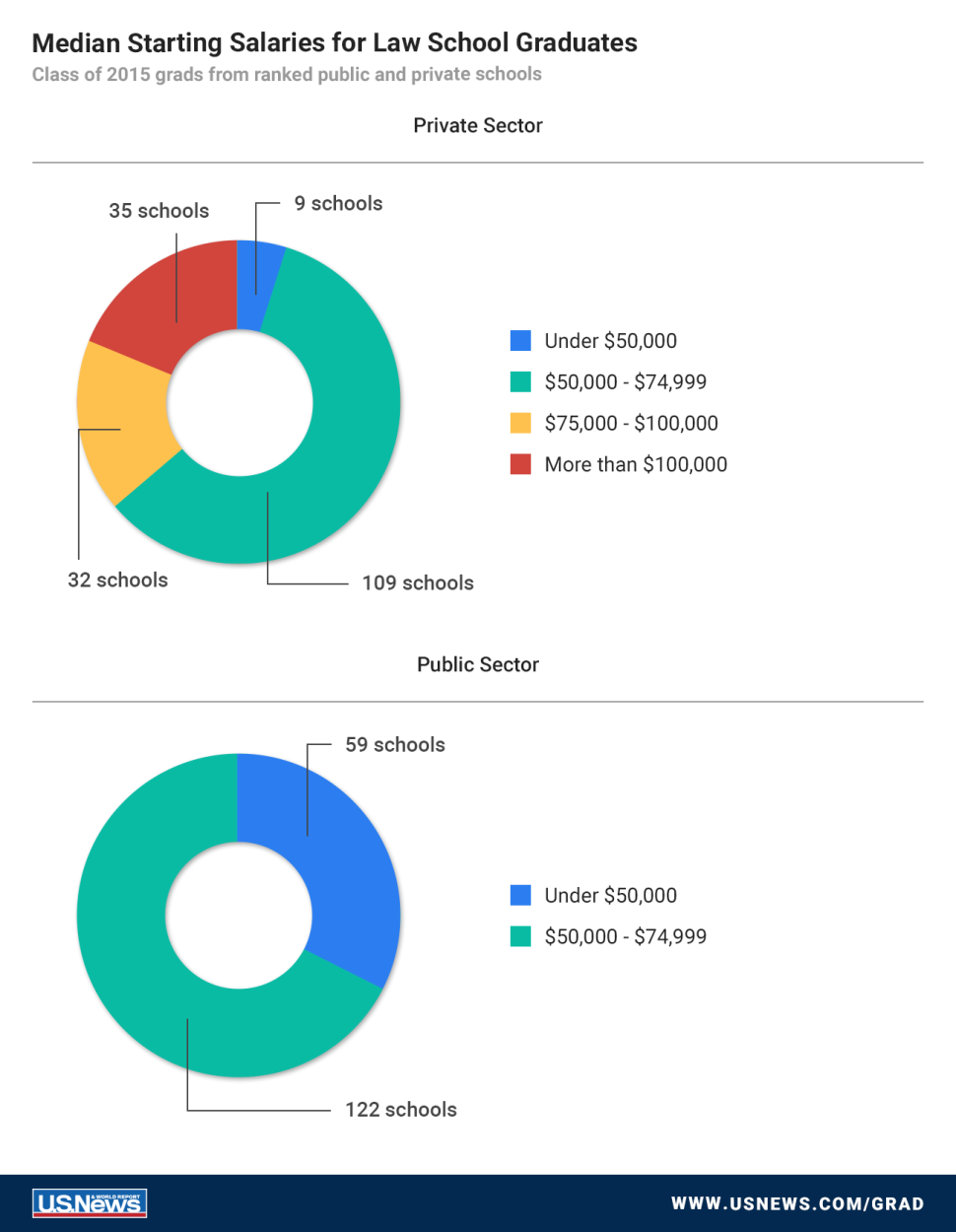

According to U.S. News & World Report, “[a]lthough six-figure starting salaries are the norm for graduates of top law schools who enter the private sector, the salaries of most newly minted lawyers aren’t even close to $100,000… Among J.D. recipients in the class of 2015 at ranked law schools, the median private sector salary was $68,300, and the median public sector salary was $52,000… The financial payoff of private sector law jobs can be enormous, especially at large corporate law firms with $160,000 [note: $180,000 as of June 2016] starting salaries. But the chance of getting one of these coveted six-figure salary jobs is slim unless you attend a law firm feeder school.”

However, for Penn Law, which is currently ranked as #7 law school in the nation (and thus qualifies as a T-14), employment and salary metrics tell a different story. Out of Penn Law’s 258 students who graduated in 2016, 253 are employed, 3 are enrolled in a full-time degree program, and 2 are seeking employment. For salaries of all job types, the 25th percentile salary is $125,000; median is $180,000; mean (average) is $149,011; and 75th percentile salary is $180,000. When looking solely at law firm salaries, the 25th percentile, median, and 75th percentile for salaries are all $180,000.

A running joke at Penn Law is that the “worst case” scenario is that you’ll land a big law job in New York paying $180K per year — maybe at a law firm you weren’t too hot about. That’s a much different calculus than being at a law school where a substantial percentage of students are unemployed upon graduation or unable to pay off their loans according to their desired timelines.

(4) Financial aid packages

Generally, top law schools offer both merit-based scholarships and need-based grants. Merit-based scholarships at Penn Law range from a few thousand dollars to full tuition. There are special merit-based scholarships for students seeking academic training and practical experience in public interest law, as well as for scholarships for Teach for America alumni and exiting corps members. Need-based grants are based on financial need as measured by FAFSA (the same financial aid application you filled out for undergrad admissions).

Just like in negotiating undergrad financial aid packages, there are strategies to leverage multiple financial aid packages from similarly ranked law schools to negotiate a better deal from your top-choice law school(s). The main caveat, however, is that this kind of negotiation will work best for schools that are similarly ranked.

How exactly does this negotiating process work? Suppose you are accepted to both Michigan Law and Penn Law (congrats!). Michigan Law offered a financial aid package that would end up with, say, $40,000 in out-of-pocket costs to you annually. Penn Law offered a financial aid package that would result in $60,000 out-of-pocket. You can contact Penn Law’s Admissions Office, emphasize that you would love to accept their offer admission (but unfortunately cannot due to financial aid reasons), and bring up that Michigan Law offered you a more favorable package. There’s a good chance that Penn will ask you to send over Michigan’s financial aid package, and Penn will match Michigan’s package (or at the very least give you some more money to narrow the gap between the two packages).

(5) External scholarships

Since my senior year of high school, I’ve been very aggressive in applying to scholarships. This was the case throughout undergrad and continues to be the case in law school. Granted, in my experience it’s a bit more tricky finding scholarship opportunities for law students compared to undergrads, but they are definitely out there.

I won’t make this sound sexier than it is — it’s very tedious and time-intensive to even find law student scholarships in the first place. You can use scholarship databases like FastWeb to start your search, but I wouldn’t stop there. I’ve found that scholarship databases are generally out-of-date (has scholarships that no longer exist or has contact information that’s outdated) and not comprehensive (missing new scholarships that have been recently created).

So, where to look? Are you doomed to dig through the Internet forever?? Not at all! Here are a few tips that, in my opinion, optimize for searching for the most valuable scholarships with the least amount of time and effort:

If you are “diverse” (a vague term of art in the law school / legal employment world), search for scholarships for women, minorities, minority women, etc. I am an Asian-American woman looking to practice in the San Francisco Bay Area, so I pay special attention to scholarships offered by affinity bar organizations, such as NAPABA (National Asian Pacific Bar Association), APABA-SV (Asian Pacific American Bar Association of Silicon Valley), and AABA-SF (Asian American Bar Association of the Greater Bay Area).

Search for scholarships specific to your law school’s region. I attend law school in Pennsylvania, so I look for Pennsylvania or Philadelphia-specific law school scholarships. Great places to start include Penn Law’s financial aid office, Drexel Law’s financial aid office, Temple Law’s financial aid office, Villanova Law’s financial aid office, etc.

If you attend law school in a region out-of-state or if you’ve lived in a certain area for a decent amount of time, check out regional scholarships that are intended for law students who are residents or former residents of the area. So, even though I currently attend law school in Pennsylvania, I’ve also lived in the Los Angeles and San Francisco Bay Areas. I’ve also lived in Central California for about five years. So, I keep an eye out for law school scholarships tied to these areas. Here, too, the best resources are law school financial aid offices that are located in these areas (e.g., UCLA Law for Los Angeles area scholarships or UC Berkeley Law for Bay Area scholarships).

There are a surprising amount of scholarships dedicated specifically for those pursuing a career in public interest law immediately after graduation. You can also search for scholarships tailored for specific areas of law, such as real estate law or tax law.

(6) Bar prep representative

As I mentioned earlier, you cannot become a licensed lawyer until you sit for your state’s bar exam and complete additional relevant requirements. And, of course, it isn’t cheap to go through this process. For example, fees to become a licensed attorney in the state of New York include a $250 application fee, a $100 “non-refundable technology fee”, a $100 laptop fee (even though you’re using your own personal laptop for the exam…), and more.

One thing I wish I knew earlier in law school is that law students can apply to represent major major bar examination prep companies (e.g., BARBRI, Themis, Kaplan) on campus and, in return, get reduced/free bar prep courses. Based on my understanding, you sit at table at school for a few hours per week and promote the company’s bar prep offerings. There are additional incentives to recruit as many of your peers as possible to your respective bar review company.

If your immediate next step after graduation is public interest (as opposed to big law, where your law firm will likely pay for bar prep and exam fees), this is an option that can save you literally a few thousand bucks in bar review fees. Just to show you what I mean… As of October 2017, BARBRI is advertising its New York state bar review course “for as low as $2695” and Themis is advertising “High-quality bar review at a reasonable price” of $2,095.

(7) Federal loan repayment assistance programs

The federal government offers four kinds of income-driven repayment plans: Revised Pay As You Earn Repayment Plan (REPAYE Plan); Pay As You Earn Repayment Plan (PAYE Plan); Income-Based Repayment Plan (IBR Plan); and Income-Contingent Repayment Plan (ICR Plan).

You may have also heard of the Public Service Loan Forgiveness Program (PSLF), which forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments (120 months = 10 years) under a qualifying repayment plan while working full-time for a qualifying employer, generally a government or non-profit employer.

Being a risk-averse person myself, I personally did not want to rely on PSLF and essentially bind myself for ten years to a loan forgiveness program that might not exist by the time my ten years are up. Since the program began in 2007, the first waves of public service loan forgiveness were theoretically set to occur in 2017. Unfortunately, there’s quite a bit of controversy (and litigation) surrounding the U.S. Department of Education’s wishy-washy position on whether it will actually honor the loan forgiveness promise it made to PSLF borrowers. At the end of the day, it’s a really crappy, uncertain position for more than half a million people who relied on PSLF in making major life and career decisions.

(8) Post-graduation student loan refinancing options

You also have the option of refinancing and consolidating your student loans. This may help you secure a lower interest rate, decrease your monthly payment, or both, depending on your individual financial situation. You can choose to refinance with the U.S. Department of Education (check out FAFSA’s FAQ on student loan consolidation for federal loans) or you can refinance with private banks. In general, it’s a good idea to refinance if you have private student loans or if you have federal student loans and don’t plan on taking advantage of a federal forgiveness program or income-driven repayment plan. You also need strong credit and a steady income to qualify for refinancing with private banks.